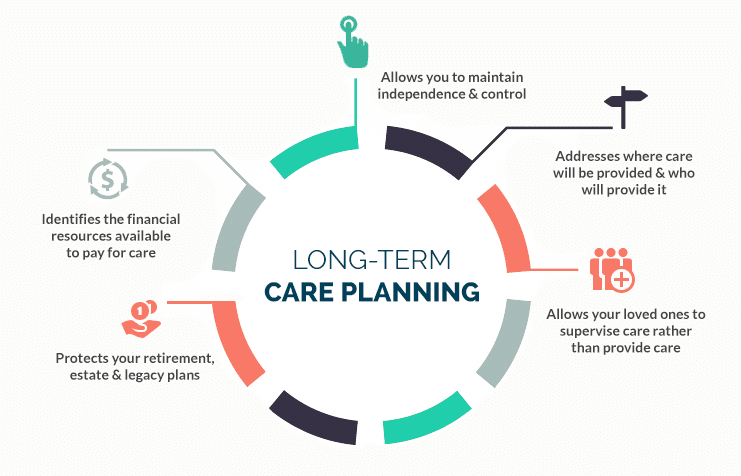

As global life expectancy continues to rise, planning for long-term care has become an indispensable component of a comprehensive financial strategy. Long-term care encompasses a range of services—from in-home assistance with daily activities to specialized nursing home care—that are often not covered by standard health insurance. The staggering cost of these services can quickly deplete a lifetime of savings, making long-term care insurance (LTCI) a critical tool for protecting assets and ensuring a dignified quality of life in one’s later years. The approach to providing and funding long-term care varies significantly around the world, reflecting different cultural norms and healthcare systems. Understanding these global perspectives is essential for anyone planning for a secure future, especially in an increasingly mobile world.

In the United States, LTCI is primarily a private insurance product, requiring individuals to proactively purchase policies. These policies can be complex and costly, making it crucial to start planning early, as premiums increase significantly with age. In contrast, countries like Germany and Japan have integrated mandatory, public long-term care insurance into their national social security systems, ensuring broader coverage for their populations. Other European nations, like the UK, utilize a hybrid model that combines state-funded support with a significant reliance on private savings and insurance. Regardless of the system, the key to effective planning is a proactive assessment of your personal health risks, family support systems, and financial resources. It is vital to carefully review policy details, such as benefit triggers, daily coverage amounts, and elimination periods, to ensure the plan aligns with your potential needs. By taking a strategic and early approach to long-term care planning, you can secure your financial future and gain peace of mind for yourself and your loved ones.